__________________

|

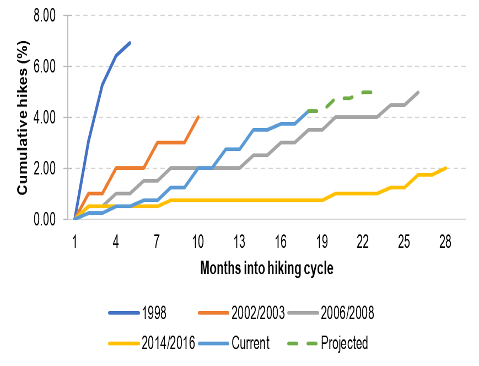

Headline CPI rose to 7.1% y/y in March from 7% in February, an increase that was slightly above consensus estimates of 6.9%. The main culprit of this increase was food price inflation that accelerated to a 14 year high of 14.4% y/y, thereby further worsening short-run inflationary impulses emanating from reduced oil supply and increasing utility costs. South Africa’s implied forward rates have since adjusted in response to the higher-than-expected CPI print. The continued rise in domestic inflation presents significant challenges to household spending which bears limited tail risks, largely constrained by high unemployment, elevated debt servicing costs, and the negative impact from persistent power outages. Notwithstanding the apparent inexistence of a demand-pull inflation in South Africa, the FRA market now expects a further 50-bps of rate hikes, with a minimum 25-bps increase pencilled-in at the next MPC meeting (see Figure 1). SA Rate Hikes

|

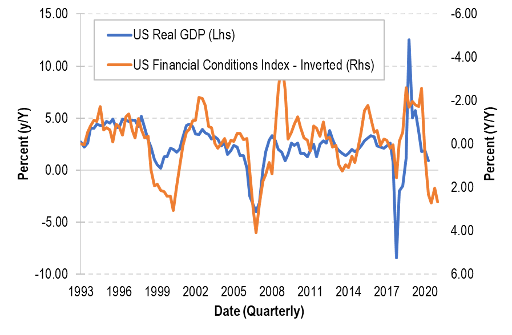

The outlook for further interest rate hikes beyond what the market is pricing in will arguably hinge on the rand and the outlook of the US monetary policy interventions. Following the Fed’s record-breaking pace of policy normalisation, U.S. headline inflation continued to moderate, easing to 5.0% y/y in March from 6.0% y/y in February. While U.S. inflation seems to have peaked, the Fed’s aggressive stance may have already taken its toll on the broader U.S. economy. Key economic data are now capitulating to tighter monetary conditions, further worsened by the Fed’s liquidity drainage and a stronger U.S. dollar. The U.S. financial conditions index, inverted and advanced by two quarters, remains strongly positively correlated with U.S. real GDP, implying slow to negative economic growth over the near term (see Figure 2). We therefore envisage that a low growth environment coupled with falling prices is likely to reduce the Fed’s hiking pace/induce a near term pivot. U.S. Real GDP YoY

|

|

In general, we remain constructive on emerging market assets which should be supported by more relaxed Covid-19 restrictions in China. The Chinese economy has rebounded faster than expected in the first quarter of the year. According to the National Bureau of Statistics, the world’s second largest economy grew at an annualised rate of 4.5% y/y in the first quarter of 2023, well above polled expectations of 4.0% y/y. The low-base recovery in China is set to provide some respite to emerging market assets, whose valuations were further undermined by a strong U.S. dollar and a negative short-term interest rate environment. After drifting well into negative territory for a prolonged period, South Africa’s real short term interest rates have recently turned positive (see Figure 3). Real short-term rates are also envisaged to grow in magnitude as the SARB looks to maintain the global hiking pace (now lagging the Fed by about 50-bps) while inflation pressures begin to moderate in the second half of the year. SA Real Short-Term Rates

|

Bottom line: our cash funds remain well positioned for the current hiking cycle, as we mainly hold floating rate instruments which will all reset their interest rate coupons to the new higher rate within the next few weeks and months. In the SA money market, the 3-m JIBAR rate rose 50 bps m/m to end the month of March at 7.958%, while the 12-m JIBAR rate increased by 18 bps m/m to 9.000%. These elevated JIBAR rates mean that money market funds are likely to generate return of between 9% and 10% over the next 12 months with no (or limited) risk of capital loss. |

Share

Press Release

13 April 2021

13 April 2021

Media Announcement: Taquanta Acquires the Entire Issued Share Capital of Ngwedi Investment Managers (NIM)

Video

25 April 2022

Optimizing Short-Term Yield- Interview with Manager of Nedgroup Investments Cash Funds

Please note Taquanta only renders financial services with clients by means of formal communication channels and does not sell or advertise any investment opportunities via social media channels such as WhatsApp or Facebook etc. Please be cautious of individuals who may fraudulently attempt to solicit business or investments by impersonating or claiming to be an associate or representative of Taquanta. If you are unsure about whether an individual is authorised to render financial services for Taquanta or not, please contact us on 021 6815100 or crm@taquanta.com to verify the identity of the individual concerned.

Ok