__________________

South Africa's economy is expected to expand below its potential growth rate over the foreseeable future. Issues such as sub-investment ratings, recurring power outages, and increasing political uncertainty, are expected to increase government’s cost of servicing debt. This situation might compel companies to make tough choices like cutting down on capital spending or reducing labour force as they grapple with deteriorating forms of public infrastructure.

In the third quarter of 2023, South Africa witnessed a 0.7 percent year-over-year contraction in its gross domestic product (GDP), contrary to the median estimate of a 0.1 percent year-over-year contraction in a Bloomberg survey. This 0.2 percent decline in output compared to the previous quarter has since raised concerns about a potential recession.

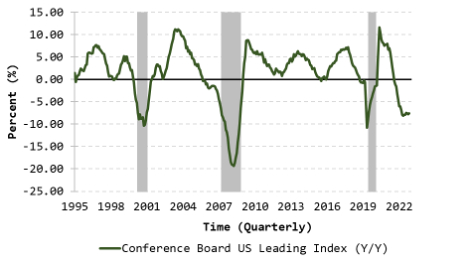

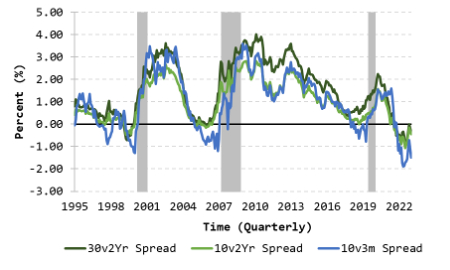

Similarly, the world's three largest economies are also experiencing a slowdown. China is contending with lower industrial activity and challenges within its property sector. The European economy faces vulnerabilities stemming from an energy crisis and decreased demand for exports. The United States (U.S.) is at risk of high interest rates on the back of bloated debt levels. Additionally, the shape of the U.S. treasury curve is also signalling an economic downturn over the near term.

|

Figure 1: Leading economic indicator

|

Figure 2: U.S. term spreads

|

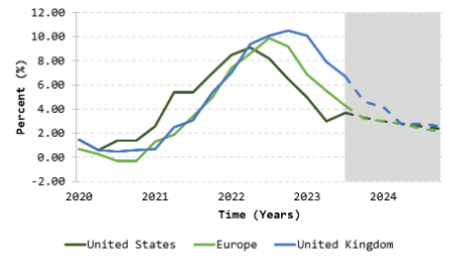

Over the last 18 months, views around inflation have been divided, however two prevailing arguments have since resolved the long-standing debate. The first is that peak inflation is now firmly behind us. The second is that inflation in many countries is starting to fall towards target.

In Europe, headline inflation fell to a 2-year low of 2.4 percent, accompanied by deflationary forces emanating from the manufacturing sector. The U.S. inflation outlook is similarly constrained by poor household savings, falling rental prices, and reduced money circulation.

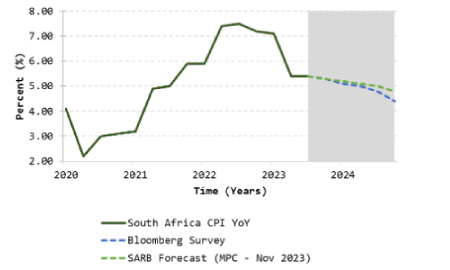

In South Africa, core inflation which excludes volatile items, hit a 15-month low in November, thereby dipping below the central bank’s midpoint target of 4.5 percent. Additionally, the Department of Mineral Resources and Energy (DMRE) announced a significant decrease in fuel prices in December, a development expected to positively impact future headline prices.

In summary, the current Consumer Price Index (CPI) outlook leans towards a downward trend. This is largely due to subdued levels of overall demand, reduced disruptions across supply chains, and declining global liquidity levels. Furthermore, a moderating macroeconomic environment is unlikely to sustain high inflationary pressures.

|

Figure 3: DM headline inflation forecasts

|

Figure 4: SA headline inflation forecasts

|

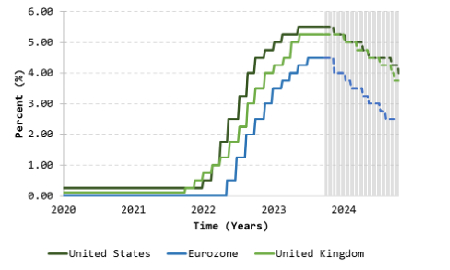

Major central banks appear to have reached the peak of their upward interest rate adjustments. The anticipation of slower economic growth and a moderation in prices is likely to mitigate the risks associated with further tightening of monetary policies. However, the commencement and pace of monetary easing will probably hinge on how swiftly economic activity and inflation respond to the economic challenges that are faced by most economies globally.

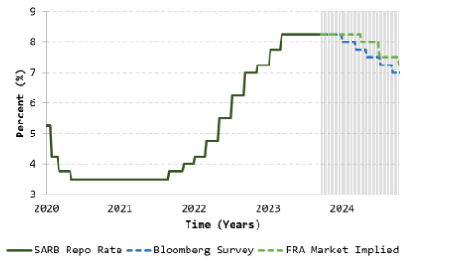

During their recent meeting, the South African Reserve Bank’s (SARB) Monetary Policy Committee (MPC) decided to leave the repo rate unchanged at 8.25 percent. The decision to pause was unanimous and in line with surveyed expectations. Policy rates remained flat in the second half of the year, spurring expectations within the interest rate market of an imminent reduction in global policy rates.

The European overnight index swaps (OIS) currently indicate an expected reduction in the policy rate of 150 basis points (bps) over the next 12 months. Conversely, in the United States, the Fed funds futures suggest an anticipated decrease of 100 basis-points in the upcoming calendar year. Similarly, the local forward rate agreement (FRA) market in South Africa estimates interest rate reductions of a comparable magnitude to those projected in the United States.

|

Figure 5: DM interest rate forecasts

|

Figure 6: SA interest rate forecasts

|

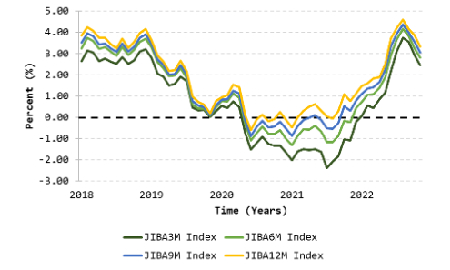

In November, the 3-month JIBAR rate saw a rise of 0.9 basis points to 8.367, whereas the 12-month JIBAR rate dropped by 22.5 basis points to 9.000 versus the previous month. Over the past year, the 3-month, and the 12-month JIBAR rates increased by 117 basis points and 41-basis points, respectively.

These elevated JIBAR rates imply that money market funds are likely to generate a return of between 9 percent and 10 percent over the next 12 months with a minimal or negligible risk of capital loss.

Despite rising expectations for lower interest rates, the delayed reset dates associated with JIBAR-linked instruments will continue to make a strong case for cash investments in both real and risk-adjusted terms. Furthermore, the absence of a strong earnings catalyst in a weaker economic environment will likely keep the market's inclination toward riskier asset classes relatively subdued.

|

Figure 5: DM interest rate forecasts

|

Figure 6: SA interest rate forecasts

|

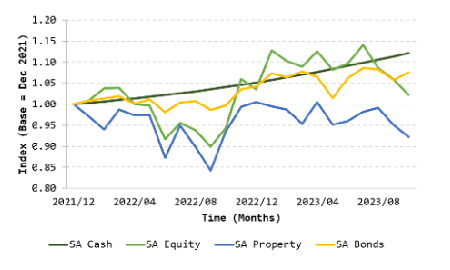

Our cash and income funds maintain a bias towards floating rate instruments, thereby immunising our portfolios against interest rate fluctuations. This strategy helps us sustain a steady level of outperformance relative to benchmarks across different evaluation periods.

Considering the anticipated cycle of rate reductions, we're gradually expanding our exposure to include some fixed-rated investments, while staying within the acceptable duration limits. In addition, we continue to look for opportunities to boost our client’s fund yield by leveraging our size, liquidity, term, or credit risk premiums, while simultaneously funding issuers at wholesale lending rates.

Share

Press Release

13 April 2021

13 April 2021

Media Announcement: Taquanta Acquires the Entire Issued Share Capital of Ngwedi Investment Managers (NIM)

Video

25 April 2022

Optimizing Short-Term Yield- Interview with Manager of Nedgroup Investments Cash Funds

Please note Taquanta only renders financial services with clients by means of formal communication channels and does not sell or advertise any investment opportunities via social media channels such as WhatsApp or Facebook etc. Please be cautious of individuals who may fraudulently attempt to solicit business or investments by impersonating or claiming to be an associate or representative of Taquanta. If you are unsure about whether an individual is authorised to render financial services for Taquanta or not, please contact us on 021 6815100 or crm@taquanta.com to verify the identity of the individual concerned.

Ok