There are two main definitions of a sovereign default. First, from a legal point of view, a default event is an episode in which a scheduled debt service is not paid beyond a grace period specified in the debt contract. Second, credit-rating agencies consider a technical default as an episode in which the sovereign makes a restructuring offer that contains terms less favourable than the original debt.

Most default episodes are followed by a settlement between creditors and the debtor government. The settlement usually takes the form of a debt exchange or debt restructuring. The new stream of payments promised by the government typically involves a structured combination of lower interest repayments, longer maturities, and a decrease in the bond principal if the default conditions are quite severe.

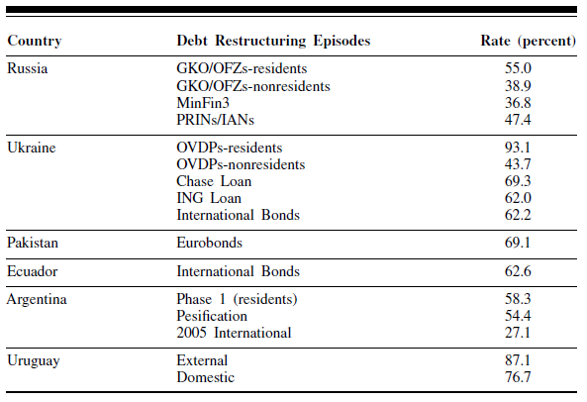

Following a debt restructure, creditors grow more inclined to estimate the recovery rates on the outstanding debt. The most commonly applied methodology computes debt recovery rates as the market value of the new instrument plus any cash received in the restructuring of the debt, divided by the net present value of the remaining contractual payments on the old instrument (inclusive of any outstanding principal or interest unpaid after the final date of maturity). The present values are often discounted using the yield of the new instrument(s). See Table 1 below.

Table 1: Average Recovery Rates Since 1998

Source: World Bank, 2005 Working Paper

Data from the World Bank shows that the average recovery rate on defaulted countries since 1998 is approximately 65% on a GDP weighted basis, with priority given to local issued bonds (i.e. domestic or residence). Except in the case of Uruguay who has a more matured external bond market, foreign currency issued bonds are usually the first tranche of sovereign debt to incur a default episode, where the recovery rate is much lower than the defaulted domestic bonds.

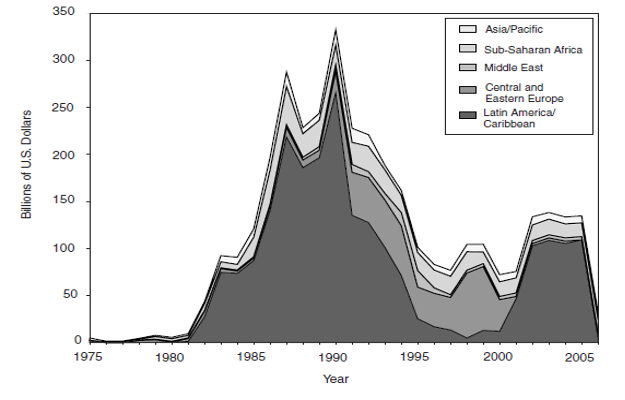

Sovereign defaults are not a novel feature in financial markets, and their incidence is widespread throughout history. For example, Spain defaulted six times between 1550 and 1650, and France defaulted eight times between 1550 and 1800. Data from the International Monetary Fund (IMF) also shows that there have been 250 documented defaults by 106 countries between 1820 and 2004. The amount of sovereign debt in default peaked at more than USD335 billion in 1990. This debt was only issued by 55 countries. See Figure 1 below.

Figure 1: Sovereign Debt in Default (1975 – 2006)

Source: IMF, 2006

Notwithstanding sovereign defaults being a common feature in financial markets, history also indicates that the determinants and effects of a default are far from being generic. Some economies are more emerging than others, while some remain more vulnerable to political turmoil and genocide attacks. The determinants of a probable default tend to influence the sovereign risk premium and the recovery rates post a default episode.

An analysis of circumstances leading to sovereign defaults is usually essential in measuring the probability of such an occurrence, and ultimately informing investment decisions. Identifying a set of states that constitutes are probable default also assists in computing or determining the appropriate price of a sovereign bond. The three main determinants of sovereign default come in the shape of: economic resources, borrowing costs, and political factors.

Economic resources:

Economic resources refer to the quantum of revenue a sovereign can generate over a given time frame. During periods of depressed economic conditions, governments tend to borrow if they do not want to decrease expenditures when tax revenue is low. This is usually premised by the smooth consumption of essential services such as: law enforcement, justice, defence, public health, public education, and other inelastic social benefits. A long recession, or equivalently, a sustained period of low tax revenue, exacerbates probabilities of a default.

Borrowing costs:

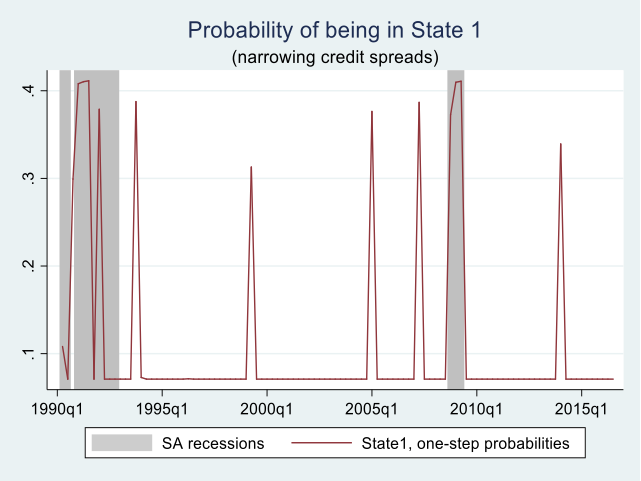

Perhaps the most pertinent cost in emerging market economies is a high inflation premium that makes it difficult for these countries to service their debt. If we adjoin this premium with deteriorating trade conditions and investment constraints to low quality debt, we ultimately reach an amplified default probability scenario. Empirical research shows that on the back of these factors, credit spreads have seldom narrowed, or equivalently, the risk premium of raising external fiscal funding has rarely decreased in almost three decades for the economy of South Africa.

Figure 2: Default Probabilities in South Africa

Source: K Leballo, University of Johannesburg

From readjusting the South African par curve with the Moody’s AAA rated par curve, the defaulting probability only marginally narrows during recessions because emerging market economies have a far greater scope to cut rates than their developed market counterparts. This is illustrated in Figure 2 where the probability of spread compression increases in a low growth and low inflation environment.

Political factors:

Political factors present themselves through the systematic risk channel, which asserts that the national budget and political influence of the ruling party tend to be under severe pressure during periods of elections and financial distress. This inclines to create systematic risks of either a disbanding in government or a change in strategic leadership, which in turn has adverse effects on economic policy as well as government’s commitment to any long-term debt obligations. However, empirical findings suggest that is not as pivotal as the liquidity of the debt instrument and the inflation risk premium.

For sovereign debt to exist, it is necessary that at least in some circumstances it would be more costly for a sovereign to default than to pay back its debt. Similarly, for sovereign defaults to exist, it is necessary that at least in some circumstances it would be more costly for a sovereign to pay back its debt than to default.

Costs imposed by creditors:

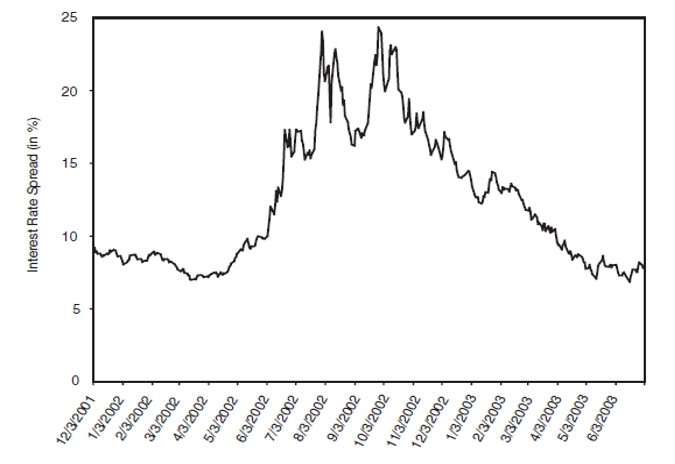

Creditors can choose to increase the borrowing cost of a “risky” sovereign so to amplify their internal rate of return in a bond that is likely to default in the future. However, increasing a defaulting sovereign’s borrowing costs would require coordination among debt holders and all other potential creditors. Such a degree of coordination seems rather unlikely to occur in liquid and competitive markets with many potential creditors. This assertion resulted in more favourable terms following Brazil’s debt restructure back in 2002.

See Figure 3.

Figure 3: Sovereign Bond Spread in Brazil

source: JPMorgan (EMBI Global)

Trade sanctions:

Research further shows that some holders of defaulted bonds can interfere with cross-border payments to other creditors who had previously agreed to a debt restructuring. If all cross-border payments could be blocked, a defaulting sovereign would not be able to borrow abroad, and no creditor would lend if it were unable to collect the payments. This does potentially lead to the exclusion from capital and goods markets in the absence of external mediation or intervention.

The intervention of a credible government or multilateral financial agency has been found to not only improve future economic prospects of a defaulting sovereign, but also recuperate the valuation of defaulted debt instruments. In 1904, Theodore Roosevelt proclaimed that the United States would intervene in the affairs of unstable Central American and Caribbean countries that could no longer repay their debts. Subsequent to this announcement, Latin American issued bonds drastically increased in value from what was once a position of paralysis.

Signalling costs:

A default decision can also signal that the policymakers in office are less prone to respect property rights of the bond holders. Slow resolutions in issues regarding maladministration and fraud may warrant persistent elevated borrowing costs post a default episode. On the other hand, if the government finds it optimal to default in recessionary circumstances, a default could signal poor economic conditions and more favourable restructuring terms. The level of accountability sovereigns take following a bailout sets the tone regarding debt holder recourse and future economic conditions (i.e. foreign direct investment openness and cross border trades).

Since the 2008/2009 financial crisis, the amount of bonds issued by governments globally increased from 1 trillion US dollars, to now a staggering 20 trillion US dollars. The United States and China account for a little over 50% of this debt, while Japan and Continental Europe make up nearly 30% of the overall outstanding bonds in issue. South Africa merely represents 0.41% of this debt book, with an average term to final maturity of 14.29 years. The primary objective of such a steep growth in global debt was for governments to engage in countercyclical investment spending, thereby resuscitate world economic activity in the aftermath of The Great Recession.

![><!--[endif]--></span></p>

<p style=](/media/o2onszvu/global-debt-landscape.png)

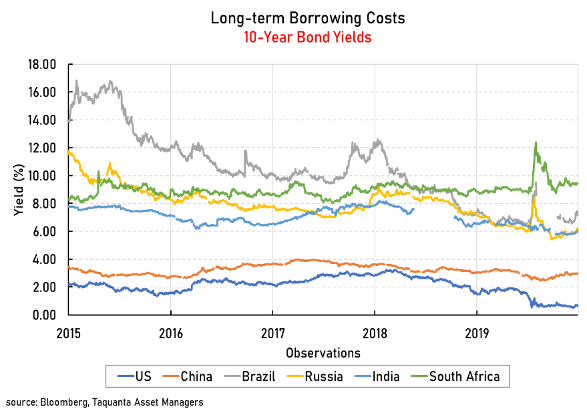

Fast forward to the year 2020, global GDP figures have averaged 2.7% in real terms since 2009, with large scale borrowers such as China and the United States averaging growth rates of approximately 7.9% and 1.8%, respectively. Despite South Africa’s comparable average growth rate of 1.4%, this figure remains well below the developed and emerging market peer averages, with its long-term borrowing costs persistently outpacing its economic growth rate.

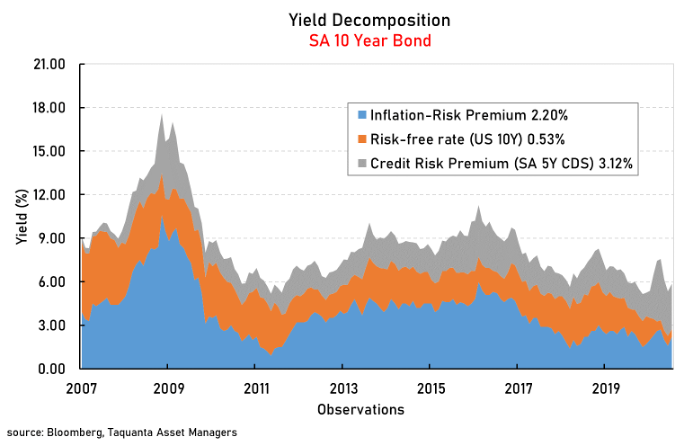

The fundamental yield decomposition of South Africa’s 10-year bond suggests that long-term borrowing costs can potentially decrease from a low inflation and low risk-free rate environment. Central banks around the world have since reaffirmed their stance on easy monetary policy remaining the global economic order until activity is firmly re-established. However, there are growing uncertainties regarding the ability of South Africa’s fiscal policy intervention in resuscitating local economic activity.

The market’s perception of this uncertainty currently outweighs the required risk premium illustrated by the credit default swap (CDS) rate. A combination of the CDS rate, risk-free rate, and the inflation risk premium suggests that fair value for SA bonds maturing in 10-years ought to be approximately 6%. In contrast, South Africa’s 10-year bonds are yielding at roughly 9%, which is 3% above both fair value and the emerging market peer average.

The South African government has been constrained with supply-side rigidities, low growth, and increasing political turmoil, which subsequently led to sub-investment credit rating downgrades by Standard & Poor’s (S&P) in 2017, Fitch in 2018, and finally Moody’s in 2020. A weaker credit rating poses a negative impact on investment spending as the cost of capital tends to increase to compensate for a higher level of investment risk.

source: National Treasury, Taquanta Asset Managers

The main concern is that this high cost of capital has been found to be tantamount to fiscal slippages, resulting in worse than expected budget deficits. Furthermore, the smooth consumption of essential services, namely: law enforcement, justice, defence, public health, public education, and other inelastic social benefits, compels the government to issue more debt, especially when economic growth and tax revenue are equally depressed.

Summary

There are numerous financial alternatives available to defaulting economies. They could exclusively issue bonds in the local market, obtain aid, or ask for conditional credit from other governments or multilateral financial institutions (i.e. IMF). It is not obvious that whether a sovereign forced to use these alternatives would face higher borrowing costs and low recovery rates.

In the case of South Africa, a low inflation regime and a few other financial aids that the country is yet to exhaust can either lead to a soft default or enable the country to completely avoid a default altogether. Also depending on the strength of the government’s strategic partnerships, either through trade blocs or local financial institutions, a high-risk economy such as South Africa, can fend off a default scenario without the risk of relinquishing its sovereignty.

Important Disclosures

TAQUANTA ASSET MANAGERS (PTY) LTD

Registration No. 1999/021871/07

(Taquanta)

Taquanta is a licensed Category I, Category II and Category IIA Financial Services Provider in terms of section 8 of the Financial Advisory and Intermediary Services Act 37, 2002 (license number 618). Accordingly, Taquanta is authorised to provide advisory and/or render discretionary intermediary services.

There are certain risks associated with investments in financial products, including market, credit & currency risks. Past performance is not necessarily an indication of future performance. All returns are rand returns, unless otherwise stated.

Taquanta Asset Managers (Pty) Ltd

P O Box 23540

Claremont, 7735

South Africa

Tel: (021) 681 5100

Share

Press Release

13 April 2021

13 April 2021

Media Announcement: Taquanta Acquires the Entire Issued Share Capital of Ngwedi Investment Managers (NIM)

Video

25 April 2022

Optimizing Short-Term Yield- Interview with Manager of Nedgroup Investments Cash Funds

Please note Taquanta only renders financial services with clients by means of formal communication channels and does not sell or advertise any investment opportunities via social media channels such as WhatsApp or Facebook etc. Please be cautious of individuals who may fraudulently attempt to solicit business or investments by impersonating or claiming to be an associate or representative of Taquanta. If you are unsure about whether an individual is authorised to render financial services for Taquanta or not, please contact us on 021 6815100 or crm@taquanta.com to verify the identity of the individual concerned.

Ok